Most products on this page are from partners who may compensate us. This may influence which products we write about and where and how they appear on the page. However, opinions expressed here are the author's alone, not those of any bank, credit card issuer, airline or hotel chain.

Choosing an account with a competitive interest rate is an easy way to grow your balance. Depending on your rate and how much you keep in your account, you could earn hundreds of dollars in interest each year. Your interest earnings could help you offset your monthly bills, boost your overall savings, or work toward a financial goal.

While it’s common to see a bank or credit union offer an interest-bearing savings account, it’s more unusual to find a checking account that earns interest. But they exist, and we’ve done the legwork of rounding up the best options for you.

Here are our top picks for interest checking accounts, how these accounts work, tips for comparing accounts, and whether this type of account is right for you.

| Account | APY | Monthly maintenance fee | Learn More |

|---|---|---|---|

|

Axos Rewards Checking Account |

Up to 3.30%

Earn up to 3.30% APY for completing qualifying activities. |

$0 |

This product is currently not available via Slickdeals. All information about this product was collected by Slickdeals and has not been reviewed by the issuer. |

|

|

Up to 0.25%

Less than $15,000 = 0.10% Annual Percentage Yield (APY). $15,000 or more = 0.25% Annual Percentage Yield (APY) |

$0 | Open Account |

|

|

Up to 0.25%

0.25% APY with $25,000 minimum balance, 0.10% APY on balances under $25,000 |

$0 | Open Account |

|

|

0.05% |

$25 with options to waive

No monthly maintenance fee when you make $5,000 in total deposits to your primary checking account each statement period OR maintain $25,000 monthly combined deposit and investment balances across your linked accounts. Otherwise a $25.00 monthly maintenance fee will apply. |

Open Account |

|

|

Up to 0.35%

0.15% on daily balances under $20,000, 0.35% on daily balances from $20,000 to $50,000 |

$10 with options to waive

Set up a monthly direct deposits of $500 or more OR maintain a daily balance of $500 or more |

Open Account |

Axos Rewards Checking Account

This product is currently not available via Slickdeals. All information about this product was collected by Slickdeals and has not been reviewed by the issuer.

- Our Rating 5/5 How our ratings work

- APYUp to 3.30%

Earn up to 3.30% APY for completing qualifying activities.

- Minimum

Deposit RequiredN/A -

Intro Bonus

Up to $500Expires July 31, 2024

Cash in on up to a $500 bonus† and up to 3.30% APY* with a new Rewards Checking account. Just use promo code RC500 before July 31.

Axos Bank Rewards Checking gives customers the chance to earn up to a 3.30% APY on their deposits with no monthly fees. These are all terrific features for a checking account, but Axos is digital-only, so if you deal with cash regularly it’s probably not the best fit for you.

Overview

While it takes a bit of work to unlock the maximum interest rate, Axos Rewards Checking customers can potentially earn an impressive 3.30% APY. This account also does not include any monthly fees.

Pros

- Strong APY compared to similar accounts

- No monthly maintenance fee or monthly minimum balance

- No overdraft or non-sufficient fund fees

- Unlimited domestic ATM fee reimbursements

Cons

- Several qualifying activities required to earn maximum interest

- No physical branch locations

Why We Like It

The Axos Bank Rewards Checking Accounts offers a competitive APY of Up to 3.30%, which is almost unheard of for a checking account. You’ll need to jump through a few hoops to earn the highest possible APY with an Axos Rewards Checking Account, but that eye-popping rate could be worth it.

APY

- Up to 3.30% APY

Features and Perks

- No monthly maintenance fees, overdraft fees, or minimum balance fees

- Up to $500 welcome bonus if you meet certain requirements, such as having an average daily balance of $7,000 and making $5,000 in qualifying direct deposits each month.

- Unlimited ATM fee reimbursements

- Debit card access

CIT Bank eChecking

Slickdeals

Why We Like It

The CIT Bank eChecking account offers minimal fees and a generous ATM reimbursement each statement cycle. Compared with some competitor accounts, this account's simple, tiered earnings structure and useful features make it a straightforward, no-fuss option.

APY

- 0.10% APY (0.10% for balances under $25,000, 0.25% for balances over $25,000)

Features and Perks

- No monthly service fees, overdraft fees, or fees for incoming wire transfers or online transactions

- Free access to CIT Bank ATMs and a $30 out-of-network ATM fee reimbursement each statement cycle

- Debit card access

- Access to Zelle, Apple Pay, and Samsung Pay

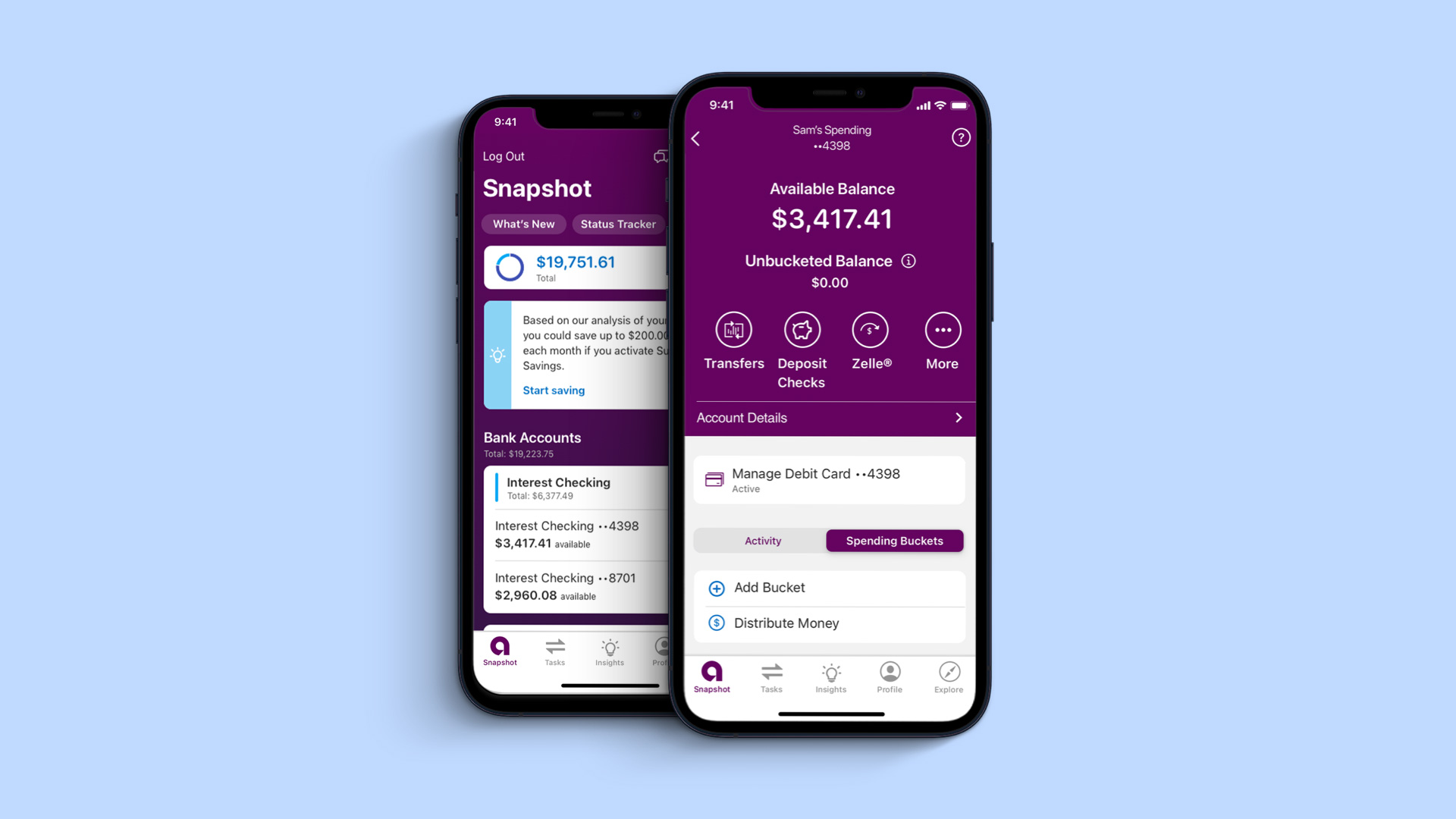

Ally Bank Spending Account

Slickdeals/Ally

Why We Like It

The Ally Spending Account is an online interest checking account with very few fees and a decent APY for balances over a certain amount. If you’re looking for help getting a handle on your finances, this account offers useful budgeting tools (like spending buckets) to help you understand and manage your spending.

APY

- Up to 0.25% APY (0.10% for balances under $15,000, 0.25% for balances over $15,000)

Features and Perks

- Free access to 43,000 AllPoint ATMs, and a $10 monthly reimbursement for out-of-network ATM withdrawals

- No monthly service fees or overdraft fees

- Budgeting tools to help you better manage your money

- Early direct deposit option

- Debit card and paper checks

Citizens Quest® Checking

Citizens

Why We Like It

The Citizens Quest® Checking account offers a lower APY than some competitors, but if you’re an existing Citizens Bank customer, opening a Quest Checking account could help you earn valuable CitizensPlus rewards. These rewards may include investment matching, a rate boost on select deposit accounts and more.

APY

- 0.05% APY

Features and Perks

- Banking with Citizens can help you earn an investment match, higher savings rate, more cash back from credit card purchases, and lucrative lending discounts.

- Monthly service fee can be waived by meeting certain requirements.

- Personalized advice from dedicated account agents.

- Debit card and paper checks

- Early direct deposit access

PenFed Credit Union Access America Checking

iStock

Why We Like It

PenFed Credit Union’s Access America Checking account offers a competitive APY rate and other perks, like overdraft protection and 2% cash back on your debit card purchases. Account holders also get 50 free paper checks and free access to a giant ATM network. You’ll need to be a member to open a PenFed Access America Checking account, but membership is open to everyone.

APY

- 0.15% on daily balances under $20,000

- 0.35% on daily balances from $20,000 to $50,000

Features and Perks

- Monthly maintenance fee can be waived by meeting certain requirements.

- Early direct deposit access

- Free and easy access to over 85,000 Allpoint and Co-op ATMs

- Cash-back debit card that lets you earn 2% back on purchases

- First 50 paper checks free

- Zelle access

- Overdraft protection

How Do Interest Checking Accounts Work?

As its name suggests, an interest checking account is a type of checking account that lets you earn a yield on your balance. It’s common to see savings accounts that earn interest—you’ll generally find one at every bank or credit union—but an interest-bearing checking account is rarer. Interest checking accounts may offer a flat earnings rate or tiered APYs, meaning that your rate may differ depending on your total account balance. Generally, the highest rates are reserved for account holders with higher balances with a tiered structure.

Online banks may be more likely to offer interest checking accounts, as these financial companies have fewer overhead costs and can often afford to pass these savings onto their customers. However, it’s possible you’ll find them with select traditional banks too.

What Is a Good Interest Rate on a Checking Account?

According to national data from the FDIC, the average checking account interest rate is 0.07% as of January 2024. Such accruals won’t add up to much, but it is still considered a return.

We consider a competitive interest rate for a checking account to be significantly higher than the national average, or anywhere from 0.15% to 0.35%. Remember, however, that checking account interest rates are variable and subject to change.

Pros and Cons of an Interest Checking Account

Pros

- Earn interest on your checking balance

- Flexible access to your money

- Savings account restrictions, like capped monthly withdrawals, don’t typically apply

Cons

- May need to meet certain balance requirements to earn the maximum APY

- Fees may apply

- Rate may not be as high as you’d get with a savings account

How to Maximize Your Money

High-interest checking accounts offer the benefits of flexibility and easy access to your money. But it can be useful to have a companion high-yield savings account too. Savings accounts may have some restrictions, such as a limited number of monthly withdrawals, but they generally come with a higher APY, meaning your money earns more interest than it would in a checking account.

To earn the most competitive yield, consider stashing your emergency fund in a high-yield savings account and your everyday spending money in a checking account. Alternatively, you could open a money market account, which offers features of both checking and savings accounts. These accounts often have higher rates than checking accounts and provide debit card access, though certain limits may apply.

Recommended High-Yield Savings Accounts

| Bank Account | APY | Features | Learn More |

|---|---|---|---|

|

|

4.85%

*Annual Percentage Yield (APY) is variable and is accurate as of 11/15/2024. Rate is subject to certain terms and conditions. You must deposit at least $5,000 to open your account and maintain $25 to earn the disclosed APY. Rate and APY may change at any time. Fees may reduce earnings. |

$5,000 min. deposit |

Open Account |

|

|

Up to 4.86%

Earn up to 4.86% APY on savings, and 0.51% APY on checking when you meet requirements. |

No minimum deposit |

Open Account |

|

Member FDIC |

0.50% - 4.00%

SoFi members with Direct Deposit or $5,000 or more in Qualifying Deposits during the 30-Day Evaluation Period can earn 4.00% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. There is no minimum Direct Deposit amount required to qualify for the stated interest rate. Members without either Direct Deposit or Qualifying Deposits, during the 30-Day Evaluation Period will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Only SoFi members with direct deposit are eligible for other SoFi Plus benefits. Interest rates are variable and subject to change at any time. These rates are current as of 12/3/24. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet. |

No minimum deposit |

Open Account |

|

|

4.55%

Earn 4.55% APY on balances over $5,000. Balances of less than $5,000 earn 0.25% APY. Annual Percentage Yield is accurate as of November 13, 2024. Interest rates for the Platinum Savings account are variable and subject to change at any time without notice. |

$100 minimum deposit |

Open Account |

How to Choose a High-Yield Checking Account

While interest-bearing checking accounts are less common than high-yield savings accounts or certificates of deposit (CDs), there’s still a decent number of accounts out there. Here’s what to consider as you compare options.

- APY: A checking account with a high APY will earn more than a checking account with a lower rate. That said, fees and other factors will also play a role in your rate of return.

- Minimum opening deposit: Some checking accounts may require a sizable minimum deposit to open a new account.

- Minimum balance requirements: Likewise, some accounts may also have an ongoing monthly minimum balance requirement, daily balance requirement, or a minimum balance to earn the highest APY possible.

- Other monthly requirements: Besides minimum balance requirements, some accounts may also have other requirements to qualify for the most competitive rates, such as enrolling in direct deposit, making one automatic deposit each month via Social Security or an annuity if you’re not employed, or making a minimum number of monthly debit card purchases.

- Account fees: Compare potential account fees, such as overdraft fees or monthly service fees.

- ATM network: A large ATM network will provide you with easier access to your money, whether you’re close to home or far away. Also look at whether the account you’re comparing offers reimbursements for out-of-network ATM withdrawals.

- Banking features and options: Look at whether the bank or credit union you’re considering offers mobile banking, in-person and online banking, and other convenient features and options.

Is an Interest Checking Account Right for You?

Opening an interest checking account can make sense if you regularly have a high balance in your checking account and you’re interested in earning money on that balance. Even if you typically keep a small balance in your checking account, it could still be a good choice, provided that you can meet your new account’s requirements to earn a competitive rate.

If you can’t meet those requirements or prefer to stay with your existing bank, it might make sense to leave your money where it is.

Jessica Ullrich

Jess is a freelance personal finance writer. She's been creating financial and business content for over a decade. Before venturing into freelance writing, Jess was on the editorial teams at Investopedia, The Balance, and FinanceBuzz. She's created content across several verticals, including budgeting, credit, debt, insurance, investing, loans, and side hustles. In her spare time, you can find Jess reading about money, working in her garden, or spending time with family.